Exploring the complex interaction between price elasticity and surplus variations provides deep insights into market behaviour and economic efficiency.

Introduction to Price Elasticity and Surplus

Understanding how price elasticity of demand and supply influences consumer and producer surplus is essential in economic analysis. These concepts help in explaining the benefits consumers and producers derive from market transactions.

Comprehensive Analysis of Consumer and Producer Surplus

Detailed Exploration of Consumer Surplus

- Consumer Surplus Defined: The economic benefit to consumers, quantified as the difference between the maximum price they are willing to pay and the market price they actually pay.

- Importance in Economics: Acts as a measure of consumer welfare and market efficiency.

- Factors Influencing Consumer Surplus:

- Price changes in the market.

- Changes in consumer preferences and income levels.

- Introduction of new products and technologies.

In-Depth Look at Producer Surplus

- Producer Surplus Explained: Represents the economic gain to producers, calculated as the difference between the market price and the minimum price at which producers are willing to sell.

- Relevance in Market Analysis: Indicates the health of the business sector and its capacity for investment and growth.

- Determinants of Producer Surplus:

- Market price fluctuations.

- Cost of production and technological advancements.

- Government policies and global market conditions.

Detailed Study of Price Elasticity of Demand

- Conceptual Understanding: It measures the degree of responsiveness of quantity demanded to changes in price.

- Elastic Demand: Characterized by a significant change in quantity demanded when price changes.

- Inelastic Demand: A scenario where quantity demanded changes minimally with price adjustments.

- Crucial Determinants:

- Availability of substitutes.

- The proportion of income spent on the good.

- Necessity versus luxury perspective.

- Time period for adjustment.

Thorough Examination of Price Elasticity of Supply

- Core Concept: Reflects how much the quantity supplied responds to a change in price.

- Elastic Supply: Indicates a significant change in quantity supplied in response to price changes.

- Inelastic Supply: Where quantity supplied is relatively unresponsive to price changes.

- Key Influencing Factors:

- Flexibility in production.

- Time period for supply adjustment.

- Availability of resources and technology.

Interaction Between Elasticity and Surpluses

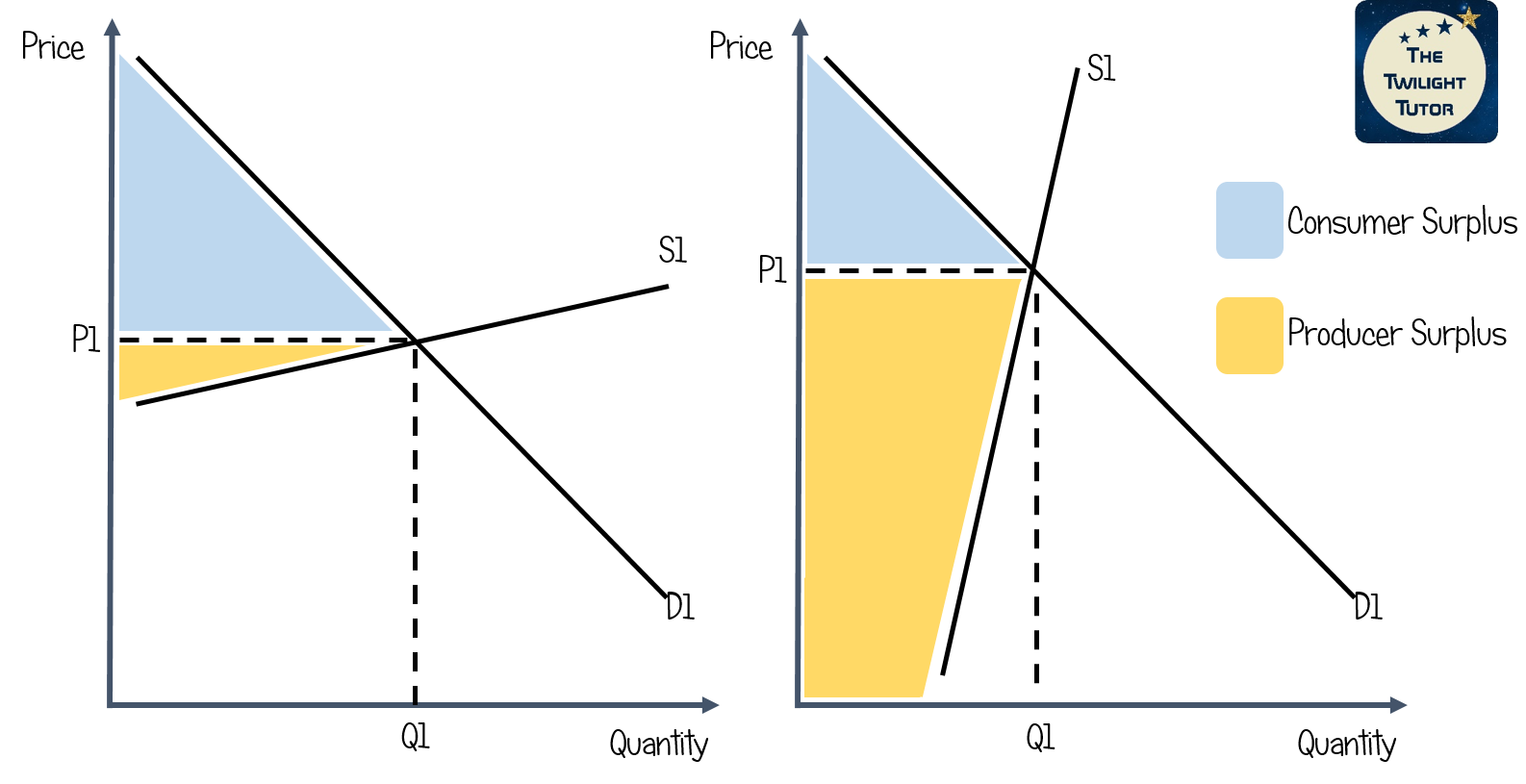

- Elastic Demand and Consumer Surplus: In markets with elastic demand, consumer surplus is highly sensitive to price changes.

- Inelastic Demand and Consumer Surplus: Here, consumer surplus is less affected by price fluctuations.

Image courtesy of tutor2u

- Elastic Supply and Producer Surplus: Markets with elastic supply witness significant changes in producer surplus with price variations.

- Inelastic Supply and Producer Surplus: In such markets, producer surplus shows minimal response to price changes.

Image courtesy of thetwilighttutor

Case Studies: Elasticity and Surplus in Diverse Markets

Case Study 1: Luxury Goods Market

- Scenario Analysis: Examining high elasticity of demand.

- Consumer Surplus Impact: Large shifts in consumer surplus with price changes.

- Practical Example: Price reductions in high-end electronics significantly increasing consumer surplus.

Case Study 2: Agricultural Sector

- Market Characteristics: Short-term inelastic supply.

- Producer Surplus Variation: Marked changes in producer surplus due to minor price adjustments.

- Real-World Example: Price surge in dairy products drastically increasing producer surplus.

Case Study 3: Technology Industry

- Market Dynamics: Characterized by both elastic supply and demand.

- Surplus Fluctuations: Noticeable effects on both consumer and producer surplus due to price changes.

- Illustrative Case: Launch of a new software platform leading to price drops in existing software, affecting surpluses.

Theoretical and Practical Implications

- Theoretical Perspectives: Elasticity concepts are fundamental in predicting and analyzing market responses and surplus variations.

- Practical Applications: These insights guide decision-making in pricing, market entry, and policy formulation.

Price Elasticity, Surplus, and Market Welfare

- Comprehensive Market Analysis: Understanding the impact of elasticity on surplus is key to assessing market welfare and efficiency.

- Indicators of Economic Efficiency: Markets showing minimal surplus fluctuations tend to be more stable and efficient.

In summary, the relationship between price elasticity and consumer and producer surplus is a vital aspect of economic theory. This relationship provides valuable insights into how market dynamics affect economic welfare. Case studies across various industries illustrate these concepts in real-world scenarios, highlighting their practical importance in business and policy decision-making.

FAQ

Market interventions such as price ceilings (maximum price limits) and price floors (minimum price limits) can significantly impact consumer and producer surplus. A price ceiling, often set below the equilibrium price, is intended to make goods more affordable for consumers. It increases consumer surplus by allowing consumers to purchase goods at lower prices than they would in an unregulated market. However, it can reduce producer surplus, as producers are forced to sell at lower prices, often leading to shortages and reduced market efficiency. Conversely, a price floor, set above the equilibrium price, is designed to protect producers, ensuring they receive a minimum price for their goods. This typically increases producer surplus by enabling higher selling prices, but it reduces consumer surplus as consumers pay more than they would in a free market. Moreover, price floors can lead to surpluses in supply, as producers are incentivized to produce more than the market demands at that price level.

Marginal utility, the additional satisfaction a consumer gains from consuming one more unit of a good or service, is closely related to consumer surplus and price elasticity. Consumer surplus occurs because consumers are willing to pay more for a good or service than what they actually pay. This surplus is rooted in the concept of diminishing marginal utility - as consumers consume more of a good, the utility gained from each additional unit decreases. Consequently, the willingness to pay for additional units decreases, creating the consumer surplus. Price elasticity of demand is influenced by changes in marginal utility. In cases where marginal utility decreases rapidly, demand tends to be more elastic because consumers are less willing to pay higher prices for additional units. Thus, a price increase leads to a significant reduction in quantity demanded, reflecting a high elasticity of demand. Understanding marginal utility helps in explaining why consumer surplus exists and how it is affected by price changes.

Externalities, which are costs or benefits incurred by third parties not directly involved in a market transaction, can significantly influence the relationship between price elasticity and surplus. In the presence of positive externalities, such as education or healthcare, the social benefit of consumption exceeds the private benefit. This discrepancy often leads to underconsumption from a societal perspective, which means that consumer surplus is less than it could be if these external benefits were internalized in the market price. Similarly, negative externalities, like pollution, result in a social cost higher than the private cost borne by producers. This often leads to overproduction and an artificially high producer surplus, as the market price does not reflect the external costs. Addressing these externalities, often through government intervention, aims to align the social and private costs/benefits, leading to a more efficient allocation of resources and a more accurate reflection of consumer and producer surplus in the market.

Yes, a good can have both elastic demand and inelastic supply. In this scenario, the quantity demanded is highly responsive to price changes, while the quantity supplied is relatively fixed in the short term. This situation often leads to volatile market conditions, especially in the face of demand shifts. For instance, if there's a sudden increase in demand, prices might rise sharply due to the inelastic supply. This price hike would significantly reduce consumer surplus since consumers are sensitive to price changes and would have to pay much more than before. Conversely, the producer surplus would increase substantially due to the higher prices. However, if the demand decreases, the reverse would happen: consumer surplus would increase due to lower prices, but producer surplus would decrease because the inelastic supply prevents producers from reducing output quickly enough to prevent price falls.

The time factor significantly influences the elasticity of supply and consequently affects producer surplus. In the short term, the supply is generally inelastic because producers cannot quickly adjust their production levels due to fixed resources and capacities. As a result, any increase in price, due to higher demand, leads to a disproportionate increase in producer surplus, as producers are selling their limited output at higher prices. Over time, as the market adjusts, producers can increase their capacity, making the supply more elastic. This increased elasticity in the long term means that a change in price will lead to a more proportionate change in quantity supplied, leading to different impacts on producer surplus. In the long run, with more elastic supply, producers can adjust production to maintain optimal surplus levels, but they also face more competition and potential price reductions, which could decrease surplus.

Practice Questions

A significant decrease in the price of a luxury good, such as designer clothing, in a market with highly elastic demand would lead to a substantial increase in consumer surplus. This is because, in such markets, consumers are highly responsive to price changes. As the price decreases, consumers who were previously unwilling or unable to purchase the product at a higher price can now do so, and those who were willing to pay more than the new, lower price gain additional surplus. This scenario illustrates the concept that in markets with highly elastic demand, consumer surplus is very sensitive to price changes.

In the agricultural sector, a sudden increase in demand for a crop, possibly due to unexpected weather conditions, can have a significant impact on producer surplus, especially in the short term where supply is inelastic. Since the supply is inelastic, producers are unable to quickly increase the quantity supplied in response to the increased demand. As a result, the market price of the crop rises. This price increase enhances producer surplus as producers sell their limited supply at a higher price. This scenario demonstrates how inelastic supply in the short term can lead to substantial increases in producer surplus when demand unexpectedly rises.