IB Syllabus focus:

'- Definition, formula'

Understanding Compound Interest

Navigating through the financial world, compound interest emerges as a pivotal concept, significantly impacting investments and loans. It's crucial to delve into its intricacies to harness its potential effectively, especially in the realm of investments, where it can substantially amplify growth over time.

The Formula for Compound Interest

The formula to calculate the future value (FV) of an investment, considering compound interest, is expressed as:

FV = PV * (1 + i/n)(n*t)

Where:

PV is the present value or initial investment/loan amount.

i is the annual interest rate (in decimal form, so 6% becomes 0.06).

n is the number of times that interest is compounded per unit t.

t is the time the money is invested or borrowed for, in years.

This formula enables us to find the future value of an investment, which is the amount of money that we will have in the future, considering the interest that compounds over time.

Practical Application

Let's delve into a practical example to comprehend the application of the formula. Suppose you invest 1000

i = 0.06

n = 12 (since the interest is compounded monthly)

t = 5

Utilizing these values in the formula, we can calculate the future value of the investment. This will give us an idea of how much the investment will grow to after 5 years, considering the compound interest. For a foundational understanding of interest calculations, consider exploring Simple Interest Basics.

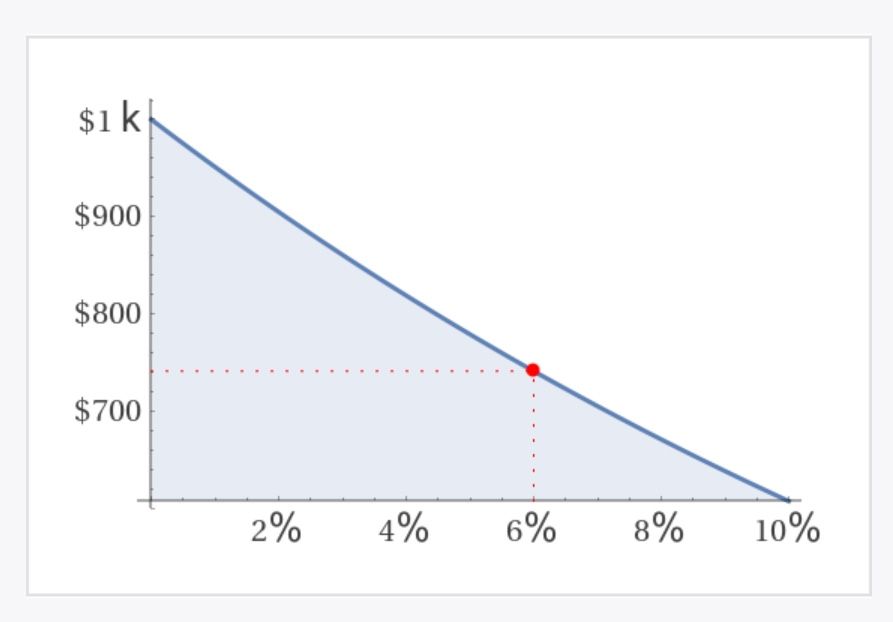

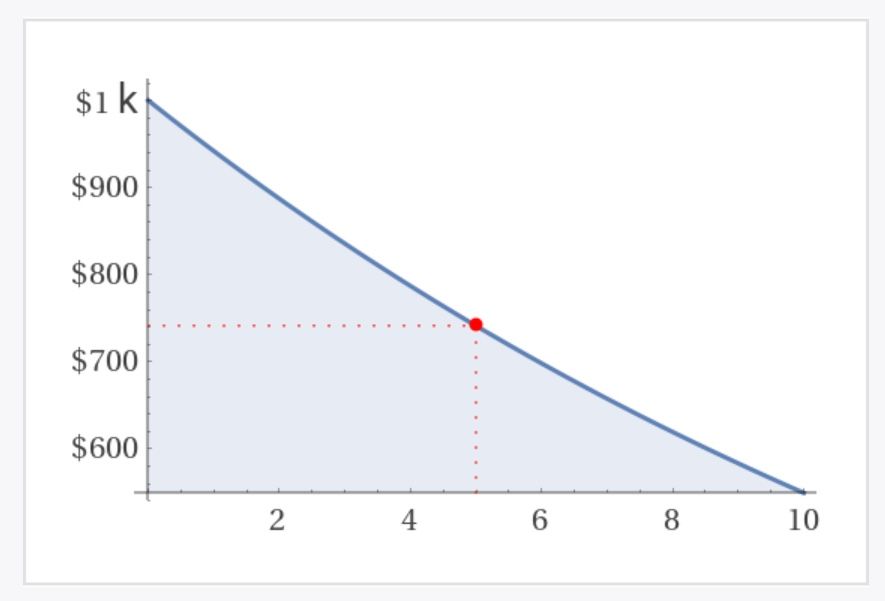

Graphical Representation

Understanding the graphical representation of compound interest can provide a visual insight into how the investment grows over time. The graph typically demonstrates how the investment evolves over different periods and at varying interest rates. For instance, a graph might depict how the present value of $1000 grows over a period of 5 years at an interest rate of 6%, providing a visual representation of the investment’s growth trajectory. The Graph Analysis page offers deeper insights into interpreting such financial graphs.

In the graph above, the x-axis could represent the interest rate, while the y-axis represents the present value. Different curves might represent different interest periods, providing a comprehensive view of how the investment matures over time under various scenarios.

Similarly, another graph might represent the present value against different interest periods, providing insights into how the length of the investment period impacts the final amount.

Significance of Compound Interest

Compound interest is significant for various reasons:

Investment Growth: It allows investments to grow exponentially over time, as the interest earned is continually reinvested. This aspect is crucial in Financial Scenarios where strategic planning can greatly influence outcomes.

Wealth Accumulation: For investors, understanding and leveraging compound interest is pivotal for wealth accumulation.

Loan Repayments: For borrowers, it’s crucial to understand how compound interest works to comprehend how much will be owed over time. This understanding is also essential when examining Interpreting Correlation between different financial variables.

The Power of Compounding

The power of compounding lies in its ability to amplify wealth over time. The longer the money is invested, the more time it has to grow, which is often referred to as the "time value of money." The concept of "the time value of money" implies that a particular sum of money in hand today is worth more than the same sum in the future due to its potential earning capacity. The principle behind this concept is further elaborated in the study of Introduction to Integrals, providing a mathematical perspective on accumulating values over time.

Factors Influencing Compound Interest

Principal Amount: The initial amount of money that is invested or loaned.

Interest Rate: The percentage of the principal that is paid as interest per period.

Time: The duration for which the money is invested or borrowed.

Compounding Frequency: How often the interest is calculated and added back to the principal amount. Understanding these factors is key to mastering financial mathematics and can be applied in various contexts, including creating financial models that predict future financial scenarios.

FAQ

The rule of 72 is a simple formula used to estimate the number of years required to double the value of an investment at a fixed annual rate of return or interest. It is directly related to the principle of compound interest as it provides a quick estimate of how an investment will grow over time. The rule states that if you divide 72 by the annual rate of return, you get the approximate number of years it will take for the initial investment to duplicate itself. For example, at a 6% rate of return, your money takes 72/6 = 12 years to double, highlighting the power and impact of compound interest in investment growth.

In the context of loans, such as a mortgage, compound interest impacts the amortisation, which is the process of spreading out the loan into a series of fixed payments. The borrower is required to pay a part of the principal and the interest in each payment. In the early years of the loan, the interest portion is larger because the outstanding balance of the loan is still high. As the principal starts to decrease, the interest portion of each payment reduces, and more of the payment is applied towards the principal. Understanding how compound interest works in amortisation helps borrowers to comprehend their repayment schedule and the actual cost of the loan over time.

Compound interest is a pivotal concept in retirement savings, acting as a catalyst in growing the savings exponentially over time. When you invest money in a retirement account, the interest earned on your initial investment (principal) also earns interest in subsequent periods, leading to a snowball effect. The longer the duration of the investment, the larger the final amount, due to the accruing interest on both the principal and the interest that has been added to it over time. Therefore, starting retirement savings early allows compound interest to significantly enhance the value of the savings, providing a larger fund in retirement.

The nominal interest rate, also known as the stated or annual interest rate, is the rate that is stated on the loan or investment without considering the effects of compounding. On the other hand, the effective interest rate does take into account the effects of compounding over a specific period of time. The effective interest rate is always equal to or higher than the nominal rate, and the difference between the two widens with the increase in the frequency of compounding. Understanding the distinction is vital for accurately comparing financial products and making informed decisions.

The frequency of compounding plays a crucial role in determining the future value of an investment or loan. The more frequently the interest is compounded, the greater the amount of compound interest will be. When interest is compounded more frequently, interest is calculated on a smaller time frame, and after each compounding period, the interest earned during that period is added to the principal, becoming the base for calculating future interest. Thus, with higher compounding frequency, the effective interest rate becomes higher, leading to a larger future value. This is particularly significant in long-term investments or loans, where the effect of compounding is more pronounced.

Practice Questions

To solve this question, we will use the compound interest formula: FV = PV * (1 + i/n)(n*t) Where:

- PV (Present Value) = £2000

- i (annual interest rate) = 0.05

- n (number of times that interest is compounded per unit t) = 12 (monthly)

- t (time the money is invested or borrowed for) = 3 years

Plugging in these values, we calculate: FV = £2000 * (1 + 0.05/12)(12*3) Calculating the values in the parentheses: FV = £2000 * (1 + 0.00416667)(36) FV = £2000 * (1.00416667)(36) FV = £2000 * 1.161112 FV = £2322.22

After 3 years, you will have £2322.22 in the account.

Again, we will use the compound interest formula: FV = PV * (1 + i/n)(n*t) Where:

- PV (Present Value) = £5000

- i (annual interest rate) = 0.06

- n (number of times that interest is compounded per unit t) = 4 (quarterly)

- t (time the money is invested or borrowed for) = 4 years

Plugging in these values, we calculate: FV = £5000 * (1 + 0.06/4)(4*4) Calculating the values in the parentheses: FV = £5000 * (1 + 0.015)(16) FV = £5000 * (1.015)(16) FV = £5000 * 1.268245 FV = £6341.23

At the end of the loan period, you will repay a total amount of £6341.23.