In the realm of market transactions, asymmetric information and moral hazard are pivotal concepts that significantly impact economic efficiency and the functioning of markets. These elements can lead to suboptimal resource allocation and various forms of market failure. This set of notes is designed to offer A-Level Economics students a thorough understanding of these concepts, their implications, and strategies to mitigate their effects.

Asymmetric Information: Definition and Types

Asymmetric information occurs when there is an imbalance in the information available to parties involved in a transaction. This imbalance can result in two key issues:

Adverse Selection

- Definition: Adverse selection is a phenomenon that occurs prior to a transaction. It happens when one party utilises their superior information to engage in a transaction that negatively impacts the other party.

Image courtesy of boycewire

- Examples and Implications:

- In insurance markets, individuals with higher health risks are more likely to purchase health insurance, leading to a pool of riskier clients and potentially higher premiums for all.

Image courtesy of wallstreetmojo

- In the used car market, sellers possessing more information about the vehicle's condition can sell lower-quality cars (lemons) at higher prices, driving good quality cars out of the market.

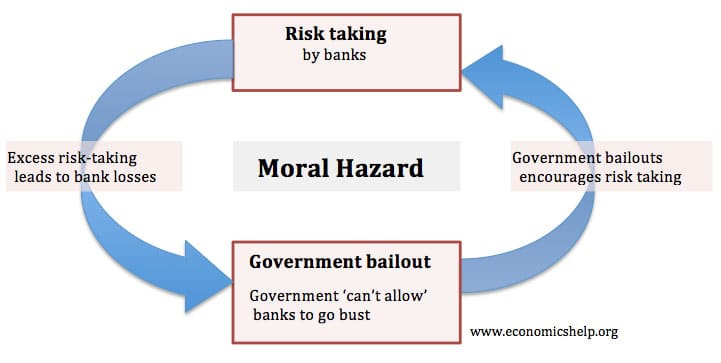

Moral Hazard

- Definition: Moral hazard arises post-transaction. It involves a party engaging in riskier behaviour because they don't bear the full consequences of that risk.

- Examples and Implications:

- In the financial sector, a bank protected by a government safety net might engage in riskier lending practices, knowing potential losses would be covered.

Image courtesy of economicshelp

- An employee with job security might exhibit decreased productivity, knowing their job is safe irrespective of performance.

Impacts of Asymmetric Information

The presence of asymmetric information can lead to various market distortions:

Market Inefficiency

- Transaction Reduction: Fear of inadequate information may cause parties to avoid participating in the market, leading to fewer transactions.

- Quality Deterioration: The inability of consumers to accurately judge the quality of products or services can lead to a decline in average quality.

Market Failure

- Lemons Problem: This concept, introduced by George Akerlof, illustrates how markets can break down completely due to asymmetric information, exemplified in the used car market where poor-quality cars dominate.

Strategies to Address Asymmetric Information

Several strategies can be employed to counter the negative effects of asymmetric information:

Signalling

- Definition and Mechanism: The informed party sends a credible signal to reveal their information. This could involve incurring costs that only a party with good-quality products or characteristics would bear.

- Examples: Academic qualifications as a signal of employee quality; warranties offered by sellers as a signal of product quality.

Screening

- Definition and Mechanism: The uninformed party undertakes actions to glean more information. This often involves setting up mechanisms that lead the other party to reveal their true characteristics or information.

Image courtesy of corporatefinanceinstitute

- Examples: Banks conducting credit checks; employers conducting background checks and interviews.

Moral Hazard: In-Depth Analysis

Moral hazard has significant implications, especially in financial markets and insurance:

Insurance and Behavioural Change

- Impact on Consumer Behaviour: Insurance can lead to changes in behaviour, as insured individuals may take more risks, assuming they are protected (e.g., less care in maintaining insured property).

Financial Markets and Risk

- Bank Behaviour and Crises: Financial institutions might engage in high-risk lending if they expect government bailouts in the event of a crisis, contributing to economic instability.

Addressing Moral Hazard

To reduce the risk and impact of moral hazard, various strategies are employed:

Incentive Alignment

- Mechanism: Creating contracts and agreements where the interests of both parties are closely aligned, reducing the incentive to act in a way that is detrimental to the other party.

- Examples: Performance-related pay in businesses; deductibles and co-payments in insurance contracts to encourage careful behaviour.

Regulatory Measures

- Government Intervention: Governments and regulatory bodies can introduce measures to control excessive risk-taking in critical sectors like banking and insurance.

Case Studies and Real-World Examples

To better grasp these concepts, examining real-world scenarios is beneficial:

Subprime Mortgage Crisis

- Asymmetric Information Role: Misleading information about the riskiness of mortgage-backed securities played a significant role in the crisis.

- Moral Hazard Aspect: Financial institutions engaged in risky mortgage lending, assuming they would be bailed out in case of a crisis.

Health Insurance Market

- Adverse Selection Dynamics: Healthier individuals opting out of health insurance, leaving a riskier pool, and potentially driving up costs.

- Moral Hazard in Action: Overutilisation of medical services by insured individuals, leading to increased healthcare costs.

Decision Analysis in the Presence of Asymmetric Information

Incorporating an understanding of asymmetric information is crucial for effective economic decision-making:

Risk Assessment in Business

- Evaluating Asymmetric Information Risks: Businesses must consider the potential for asymmetric information in their strategic planning, assessing the likelihood and impact of adverse selection and moral hazard.

Policy Formulation and Implementation

- Government Policy Design: Policymakers need to address both adverse selection and moral hazard through regulation, incentives, and information provision to ensure efficient market functioning.

By exploring asymmetric information and moral hazard in depth, students can gain a nuanced understanding of these concepts, preparing them to analyse real-world economic scenarios and contribute to informed economic and policy debates.

Practice Questions

In the context of health insurance, moral hazard occurs when insured individuals change their behaviour because they do not bear the full cost of their actions. An excellent A-Level Economics student would explain that when individuals are covered by health insurance, they might engage in riskier health behaviours or overutilise medical services. This is because the insurance coverage shields them from the financial consequences of their actions. For instance, an insured person might opt for more medical tests or treatments than necessary, as they are not directly bearing the full cost. This behaviour can lead to inefficiencies in the healthcare market, such as increased healthcare costs and strain on medical resources.

Adverse selection can lead to market failure in the used car market, a phenomenon famously described as the 'Lemons Problem' by economist George Akerlof. In this market, sellers have more information about the quality of the car than buyers. Sellers of high-quality cars ('peaches') are unable to get a fair price due to the buyer's inability to distinguish between good quality and poor quality cars ('lemons'). Consequently, 'peaches' are driven out of the market, leaving only 'lemons'. This scenario demonstrates how adverse selection can result in a market dominated by low-quality goods, leading to market failure. The presence of asymmetric information between buyers and sellers results in inefficient market outcomes and a loss of welfare.

FAQ

Asymmetric information in the labour market can significantly affect employment and wage dynamics. Employers often face uncertainty regarding the true skills, capabilities, and work ethic of potential employees. This uncertainty can lead to inefficiencies in hiring processes and wage determination. Employers might respond to this uncertainty by offering lower wages than they would if they had complete information, or they might overemphasize credentials and experience as proxies for productivity, potentially overlooking capable candidates. This can result in a mismatch between job requirements and employee skills, leading to underutilisation of the workforce and decreased job satisfaction. Furthermore, employees with less visible skills or non-traditional backgrounds may face difficulties in proving their value, leading to underemployment or unemployment. On the other side, employees may have inadequate information about the working conditions, company culture, or future prospects of a job, leading to suboptimal job choices. These dynamics can contribute to wage disparities and inefficiencies in the allocation of labour in the economy.

Technology can significantly mitigate the problems of asymmetric information in several ways. First, the internet and digital platforms have greatly increased the availability and accessibility of information. Online reviews, rating systems, and comparison websites empower consumers with information about products and services, reducing the knowledge gap between buyers and sellers. For example, in the hospitality industry, websites like TripAdvisor provide customer reviews and ratings, helping potential customers make informed decisions. Secondly, blockchain technology, particularly in financial services, offers enhanced transparency and security, reducing the risks associated with asymmetric information. Smart contracts and decentralized finance (DeFi) platforms can automate and securely record transactions, making information readily available and verifiable. Finally, advancements in data analytics and AI enable better risk assessment and fraud detection, particularly in insurance and banking sectors. These technologies can analyse large volumes of data to identify patterns and risks, improving the accuracy of information available to both providers and consumers.

Yes, asymmetric information can lead to underinvestment in certain markets. This typically occurs when potential investors lack sufficient or accurate information about the investment opportunities or the risks involved, leading to a higher perceived risk and subsequently lower investment. For example, in the context of financial markets, if a company seeking investment cannot credibly convey its true potential or the risks involved, potential investors might be unwilling to invest, fearing that the investment is riskier or less profitable than it actually is. Similarly, in the venture capital market, investors might be reluctant to invest in start-ups due to the difficulty in accurately assessing their potential and risks. This underinvestment due to asymmetric information can lead to a lack of funding for potentially profitable projects, slowing down innovation and economic growth. It can also lead to a concentration of investment in established companies or sectors, exacerbating economic inequalities and reducing overall market efficiency.

Government regulation plays a crucial role in reducing the impact of asymmetric information. Regulatory measures are designed to increase transparency, ensure fairness, and protect consumers from the adverse effects of information imbalances. One common form of regulation is the requirement for full disclosure of information. For instance, financial regulations often require companies to disclose detailed financial information to ensure that investors can make informed decisions. Another approach is the establishment of quality standards for products and services, which helps to reduce the quality uncertainty that consumers face. Regulations on labelling, for instance, compel manufacturers to provide accurate information about the contents and features of their products. Additionally, professional licensing and certification requirements in sectors like healthcare and education ensure that only qualified individuals provide certain services, thereby reducing the risk of asymmetric information. However, it's important to strike a balance as excessive regulation can lead to increased costs and reduced incentives for innovation and market participation.

Asymmetric information can significantly impact consumer choice in markets by limiting the information available to consumers, leading to suboptimal decision-making. When one party, typically the seller, has more or better information about a product or service than the consumer, it creates a situation where the consumer cannot accurately assess the value or risk associated with the product. For example, in the market for electronic goods, consumers may struggle to understand the technical specifications and long-term reliability of products. As a result, they might either overpay for a product, thinking it's of higher quality than it is, or underpay for a product, missing out on better features that justify a higher price. This imbalance in information can lead to the selection of inferior products, reduced consumer welfare, and overall market inefficiency. Businesses might exploit this by marketing inferior products as superior, leading to a misallocation of resources and a loss of trust in the market.