In the realm of economics, scarcity is a core concept that drives the dynamics of resource allocation and decision-making. This segment delves into the nuances of scarcity, shedding light on its implications for individuals, firms, and governments.

Understanding Scarcity as a Central Economic Problem

Scarcity, fundamentally, is the condition where the available resources are insufficient to satisfy all human wants and needs. This imbalance is the cornerstone of economic studies.

- Nature of Resources: Resources in economics refer to anything that has utility and includes natural resources, human resources, and capital. The scarcity of these resources is a universal reality, affecting every economy.

- Unlimited Wants vs Limited Resources: The crux of scarcity lies in the paradox of having limitless wants in a world of limited means. This endless desire for more sets the stage for the crucial economic problem of how to allocate scarce resources effectively.

- The Pervasiveness of Scarcity: Scarcity is not just a problem for the poor or underdeveloped nations; it is a universal economic issue. Even the wealthiest societies face scarcity as they decide how to allocate their resources.

Image courtesy of ukessays

Exploration of Why Resources Are Limited

Delving deeper into why resources are limited, several factors come into play:

- Physical Limitations: The planet has physical limits. Natural resources like minerals, oil, and even atmospheric capacity have bounds.

- Sustainable Usage: Overuse of resources leads to depletion and environmental damage, further exacerbating scarcity.

- Technological and Human Capacity: The level of technology and the skills of the workforce can limit the efficient use of resources. Advances in technology can sometimes alleviate scarcity but also create new demands.

- Distribution and Accessibility: Sometimes, scarcity is more a matter of distribution and accessibility rather than absolute shortage. Political, social, and economic barriers can restrict access to abundant resources.

Impact of Scarcity on Societies and Economies

The implications of scarcity are profound and multifaceted:

- Resource Allocation: Scarcity forces societies to decide how to distribute resources optimally. These decisions are not just about quantities but also about the quality and types of goods and services to be produced.

- Opportunity Cost and Trade-offs: Every choice made due to scarcity involves an opportunity cost. This concept is central to understanding economic decision-making. It's about what is given up in order to obtain something else.

- Influence on Economic Systems: Scarcity is a key reason for the existence of different economic systems (capitalism, socialism, etc.). These systems provide frameworks for making decisions about resource allocation.

- Social Implications: Scarcity often leads to inequality. How resources are allocated can significantly impact the distribution of wealth and opportunities within a society.

- Innovation and Efficiency: Scarcity can drive innovation as societies strive to use resources more efficiently or find alternatives.

Scarcity in Practice: Real-world Examples

Illustrative examples of scarcity in various contexts:

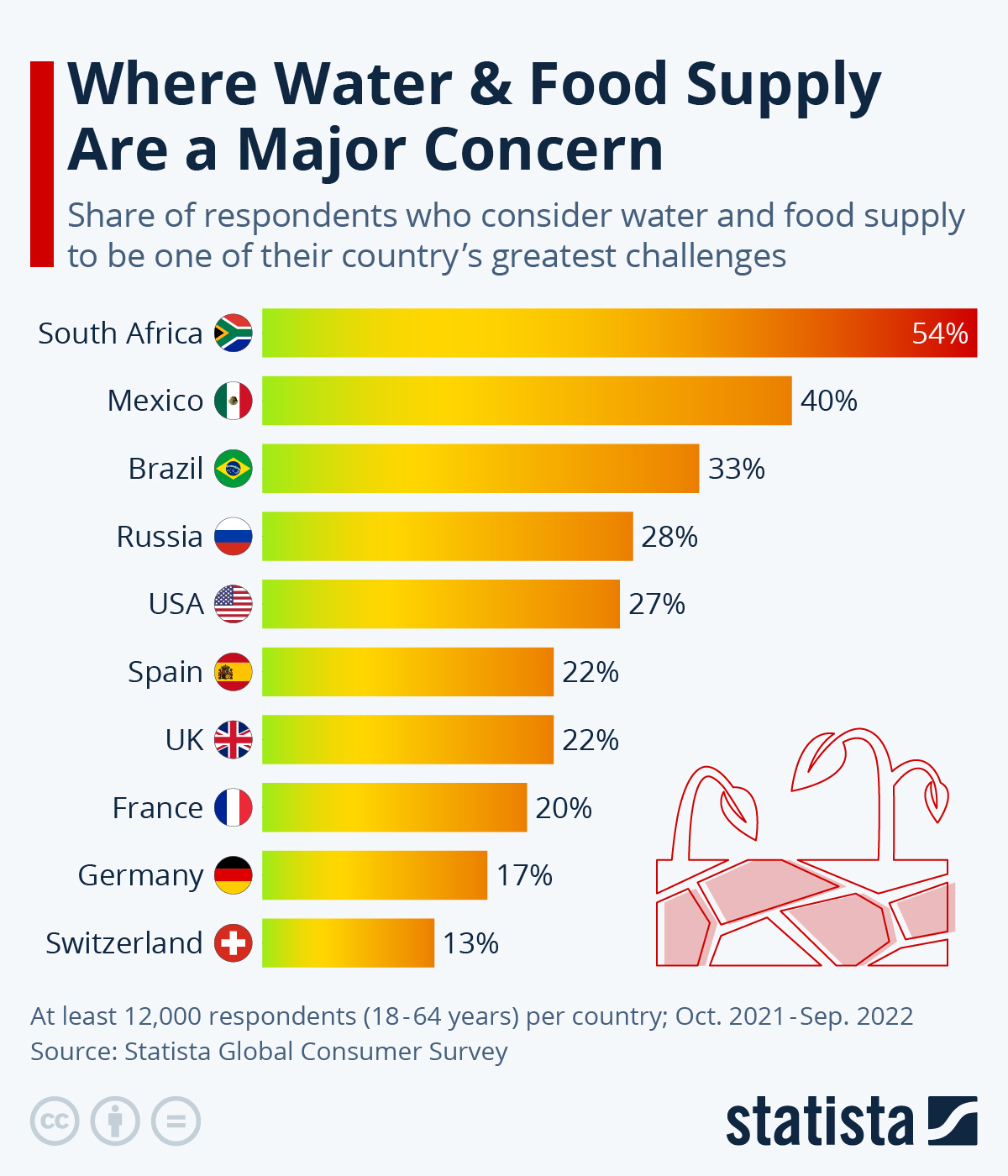

- Food Scarcity: Despite global advancements, food scarcity remains a critical issue. Factors like climate change, war, and economic instability exacerbate this problem, leading to hunger and malnutrition.

Image courtesy of statista

- Healthcare Resources: The scarcity of healthcare resources, especially in times of crisis like pandemics, highlights the need for effective allocation strategies. Deciding who gets access to limited medical care or vaccines is a stark example of scarcity at play.

- Education and Skilled Labour: The limitation in educational resources and skilled labour affects economic growth and development. Decisions about investing in education and training are influenced by these scarcities.

Addressing Scarcity: Economic and Policy Responses

Various strategies are employed to manage scarcity:

- Economic Planning and Forecasting: Governments and organisations use economic planning and forecasting to anticipate and manage resource scarcity.

- Market Mechanisms: In market economies, prices often act as signals of scarcity, guiding the allocation of resources.

- Innovation and Technology: Technological advancements can alleviate scarcity by improving efficiency and creating substitutes.

- International Cooperation and Trade: Countries often engage in trade to overcome their resource limitations, importing what they lack and exporting abundances.

Conclusion

In essence, scarcity is a fundamental economic problem with far-reaching implications. It dictates how resources are allocated, influences policy decisions, and shapes the structure of economies. For A-Level Economics students, understanding scarcity is crucial for comprehending broader economic principles and their applications in real-world scenarios.

FAQ

Eliminating scarcity in its entirety is practically impossible because the fundamental nature of scarcity stems from unlimited human wants versus limited resources. As society advances, new wants and needs emerge, continuously creating new forms of scarcity. Even in highly developed economies, where basic needs like food and shelter are largely met, scarcity manifests in more complex forms, such as the scarcity of luxury goods, advanced healthcare, or even leisure time. Advances in technology and increases in production can alleviate some aspects of scarcity, but they often give rise to new desires and needs. For instance, the advent of the internet reduced information scarcity but created a new demand for digital services and faster connectivity. Therefore, scarcity is a dynamic and ever-evolving challenge that economies continuously strive to manage, rather than fully overcome.

Environmental factors contribute significantly to economic scarcity in several ways. Firstly, natural resource depletion, such as the overuse of fossil fuels, water, and deforestation, leads to a reduction in the availability of these vital resources, creating scarcity. Secondly, environmental degradation, such as pollution and climate change, can diminish the quality and quantity of resources. For example, soil erosion reduces arable land, affecting agricultural productivity and leading to food scarcity. Thirdly, extreme weather events, exacerbated by climate change, can destroy resources and infrastructure, creating immediate and long-term scarcity. These environmental challenges require economies to adapt and innovate, finding sustainable ways to manage and use resources, highlighting the interconnectedness of environmental health and economic sustainability.

Scarcity significantly impacts consumer behaviour in various ways. Firstly, it creates a sense of urgency and can drive consumers to purchase products more quickly, especially if they perceive that a product is in limited supply. This is often seen in marketing strategies that use limited-time offers or limited-edition products to create a sense of scarcity. Secondly, scarcity can lead to prioritisation where consumers choose essentials over luxuries, especially in times of economic downturn or personal financial constraints. Lastly, scarcity can also influence the perceived value of goods; items that are scarce are often seen as more valuable. This perception can lead consumers to pay higher prices for rare items, influencing market dynamics and pricing strategies.

Scarcity plays a pivotal role in shaping global trade and international relations. Countries rich in certain resources but scarce in others engage in trade to balance these disparities. For instance, a country with abundant oil reserves but limited agricultural land will export oil and import food. This interdependence can foster cooperative relationships and economic partnerships. However, competition for scarce resources can also lead to conflicts and strained relations, particularly when resources like oil, water, or minerals are involved. Additionally, scarcity can drive nations to explore and invest in alternative resources, influencing global economic trends and technological advancements. For example, the scarcity of fossil fuels has spurred investments in renewable energy, reshaping global energy markets and alliances.

The concept of scarcity is directly applicable to personal finance and budgeting. Just as resources are limited in the economy, an individual's financial resources, such as income, are limited. Budgeting is essentially an exercise in addressing scarcity. Individuals must prioritise their spending according to their needs and wants, understanding that allocating money to one area (like leisure) means less for others (such as savings or investment). This prioritisation reflects the economic principle of opportunity cost, where choosing one alternative means forgoing another. Effective budgeting, therefore, requires making informed choices about how to allocate limited financial resources in a way that maximises personal welfare and long-term financial stability. For example, choosing to save for retirement or invest in education can have long-term benefits, despite the immediate sacrifice of not spending on immediate desires.

Practice Questions

Scarcity, the fundamental economic problem, arises because resources are limited while human wants are unlimited. This discrepancy necessitates choices as societies cannot satisfy all wants simultaneously. For instance, a government may have to choose between investing in healthcare or education. Investing more in healthcare might mean less funding for education, illustrating the opportunity cost. Excellent economic decision-making involves evaluating these trade-offs to maximise benefits from limited resources. Thus, scarcity dictates that every choice has an associated cost, guiding how resources are allocated in an economy.

Resource scarcity significantly influences a country's economic policies. For example, a country with scarce natural water resources, like Egypt, must formulate policies that prioritize water conservation and efficient usage. This might include investing in desalination plants, implementing strict usage regulations, and encouraging water-saving technologies. Such policies aim to manage the limited resource effectively, ensuring sustainable use for future needs. This scenario demonstrates how scarcity compels governments to make strategic decisions, balancing current demands with long-term resource availability, highlighting the critical role of economic planning in addressing scarcity challenges.