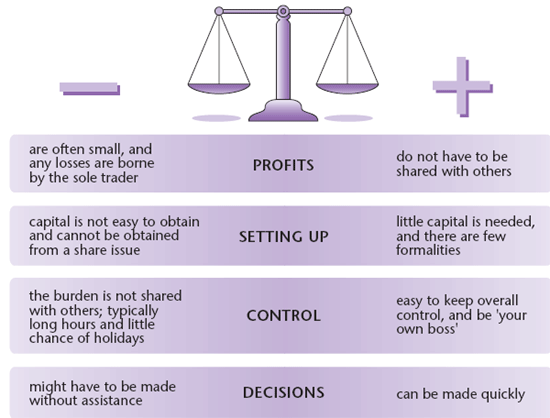

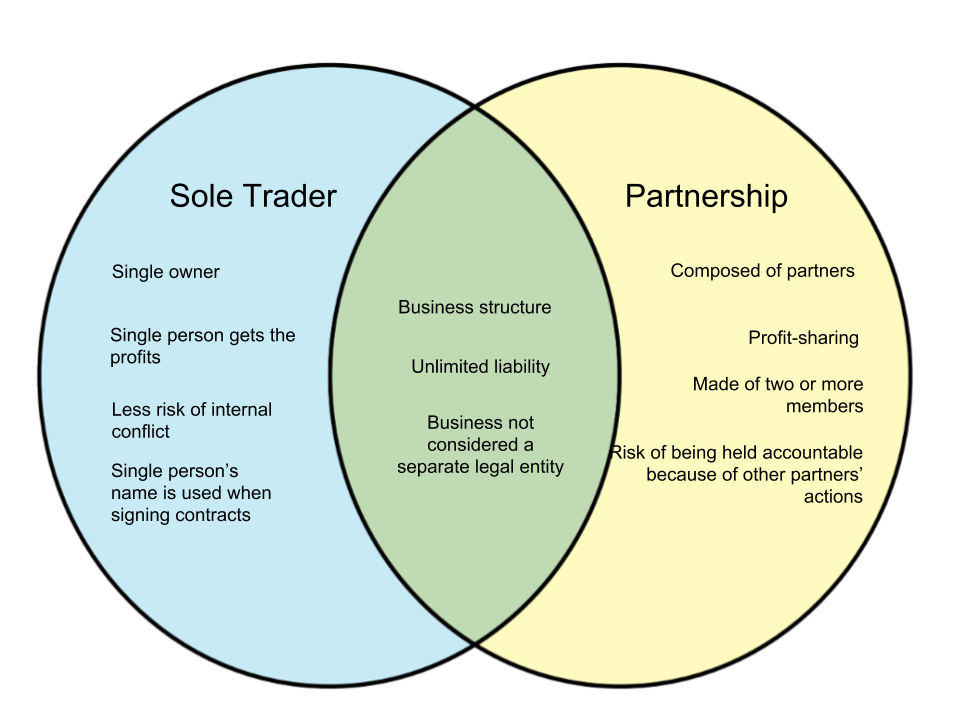

Sole Traders

A sole trader is an individual who owns and runs their business. It is the simplest and most common form of business ownership.

- Characteristics:

- Single Ownership: The business is entirely owned and controlled by one person, offering simplicity in decision-making and operations.

- Unlimited Liability: The owner is personally responsible for all business debts and liabilities. This means personal assets can be used to pay off business debts.

- Autonomy in Decision-making: The owner has complete control over the business, including decisions about operations, finances, and business direction.

- Simple to Establish and Operate: Fewer legal formalities and lower start-up costs compared to other business structures.

- Taxation: Profits are treated as the owner’s personal income and taxed accordingly.

- Suitability: Best for small-scale businesses or those just starting. Ideal for entrepreneurs who prefer full control and have a manageable level of business risk.

Image courtesy of revisionworld

Partnerships

Partnerships involve two or more individuals managing and operating a business together.

- Characteristics:

- Shared Ownership and Responsibility: Partners share the management and financial responsibilities of the business.

- Unlimited Liability: Like sole traders, partners are jointly and severally liable for the debts of the business.

- Decision-making and Profit Sharing: Decisions and profits are typically shared equally among partners, though agreements may vary.

- Partnership Agreement: A legal document outlining the roles, responsibilities, profit-sharing ratios, and other operational details of the partnership.

- Tax Considerations: Each partner pays tax on their share of the profits.

- Suitability: Suited for professional services like law firms or accountancy practices. It’s important for potential partners to have trust and a clear agreement to avoid conflicts.

Image courtesy of diff.wiki

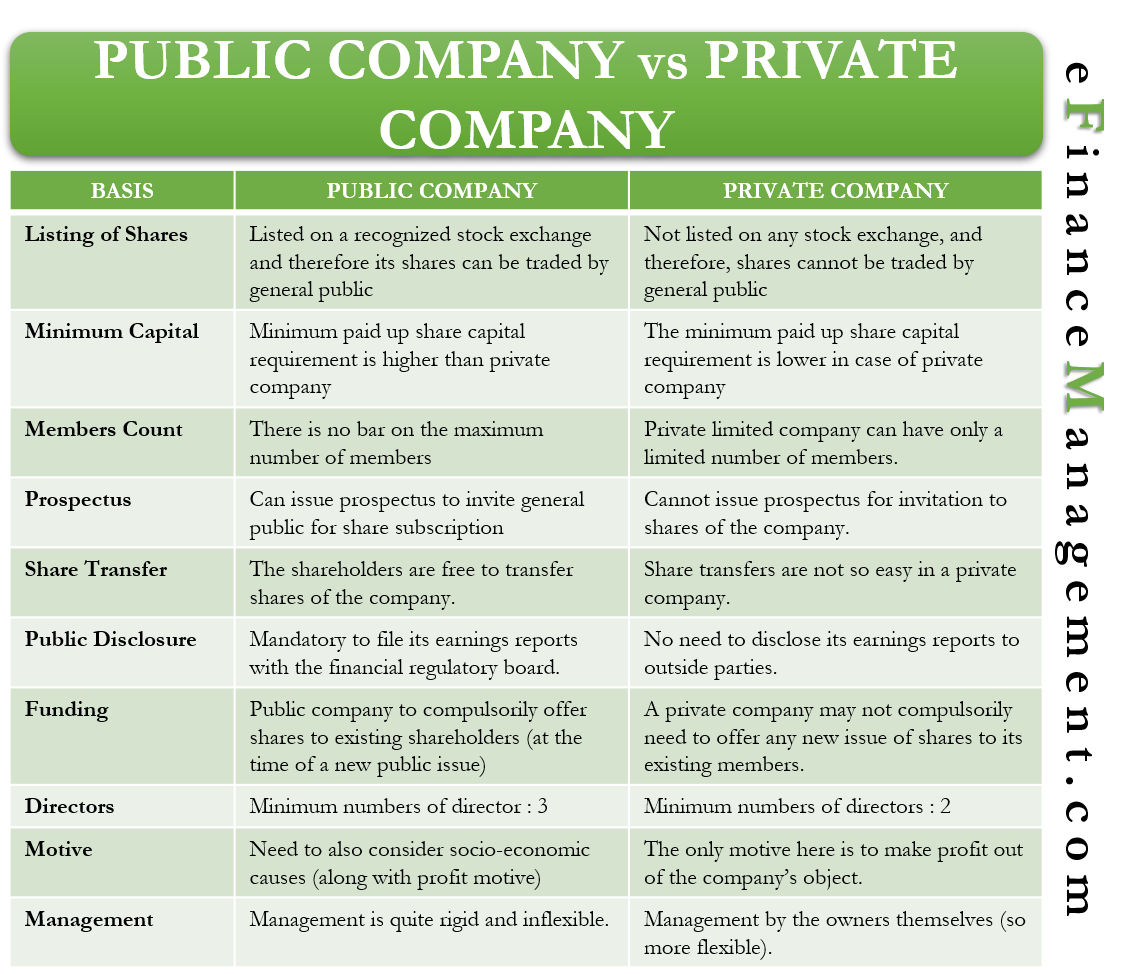

Private Limited Companies (Ltd)

Private limited companies are more complex structures, offering benefits like limited liability.

- Characteristics:

- Limited Liability: Shareholders’ liability for debts is limited to their investment in the company.

- Ownership through Shares: Owned by one or more shareholders who are often also directors.

- Separate Legal Entity: The company has its legal personality, which means it can own property, sue, and be sued.

- Profit Distribution through Dividends: Profits distributed to shareholders in the form of dividends.

- Regulation and Reporting: Subject to stricter regulatory requirements and must file annual accounts.

- Suitability: Ideal for businesses that need to raise capital but wish to retain control over who can buy shares. Offers protection to owners’ personal assets.

Public Limited Companies (PLC)

PLCs can offer shares to the public and are typically larger, more established companies.

- Characteristics:

- Limited Liability for Shareholders: Shareholders are liable only up to the amount they have invested.

- Ability to Raise Capital through Public Shareholders: Can sell shares on the stock market, providing significant capital-raising opportunities.

- Governance and Regulation: Subject to rigorous regulatory requirements, including detailed financial reporting and governance standards.

- Board of Directors: Managed by a board responsible for major company decisions and strategies.

- Suitability: Suitable for large-scale businesses looking for substantial capital investment and those willing to comply with the extensive disclosure and governance requirements.

Image courtesy of efinancemanagement

Franchises

Franchising allows a business to expand by granting others the license to operate using its brand and business model.

- Characteristics:

- Franchise Agreement: A contract between the franchisor (the original business) and the franchisee (the individual or group using the brand).

- Brand and Operational Consistency: Franchisees must adhere to specific operational and quality standards to maintain brand integrity.

- Initial Investment and Ongoing Fees: Franchisees pay initial fees and ongoing royalties.

- Training and Support: Franchisors typically provide training, support, and resources to franchisees.

- Suitability: Good for those who want to run a business with an established brand and operational model. However, franchisees have limited operational autonomy.

Image courtesy of franchisedirect

Co-operatives

Co-operatives are member-owned and democratically controlled businesses that operate for the benefit of their members.

- Characteristics:

- Democratic Member Control: Each member, regardless of their investment size, has one vote in decision-making.

- Shared Ownership and Profits: Members share in the ownership, decision-making, and profits.

- Community or Member Focus: Often oriented toward serving the needs of members or a specific community.

- Variable Structure: Can take various legal forms, including worker, consumer, or producer co-operatives.

- Suitability: Ideal for groups with common goals or interests who value democratic control and a focus on member or community benefits.

Image courtesy of prairieenergy

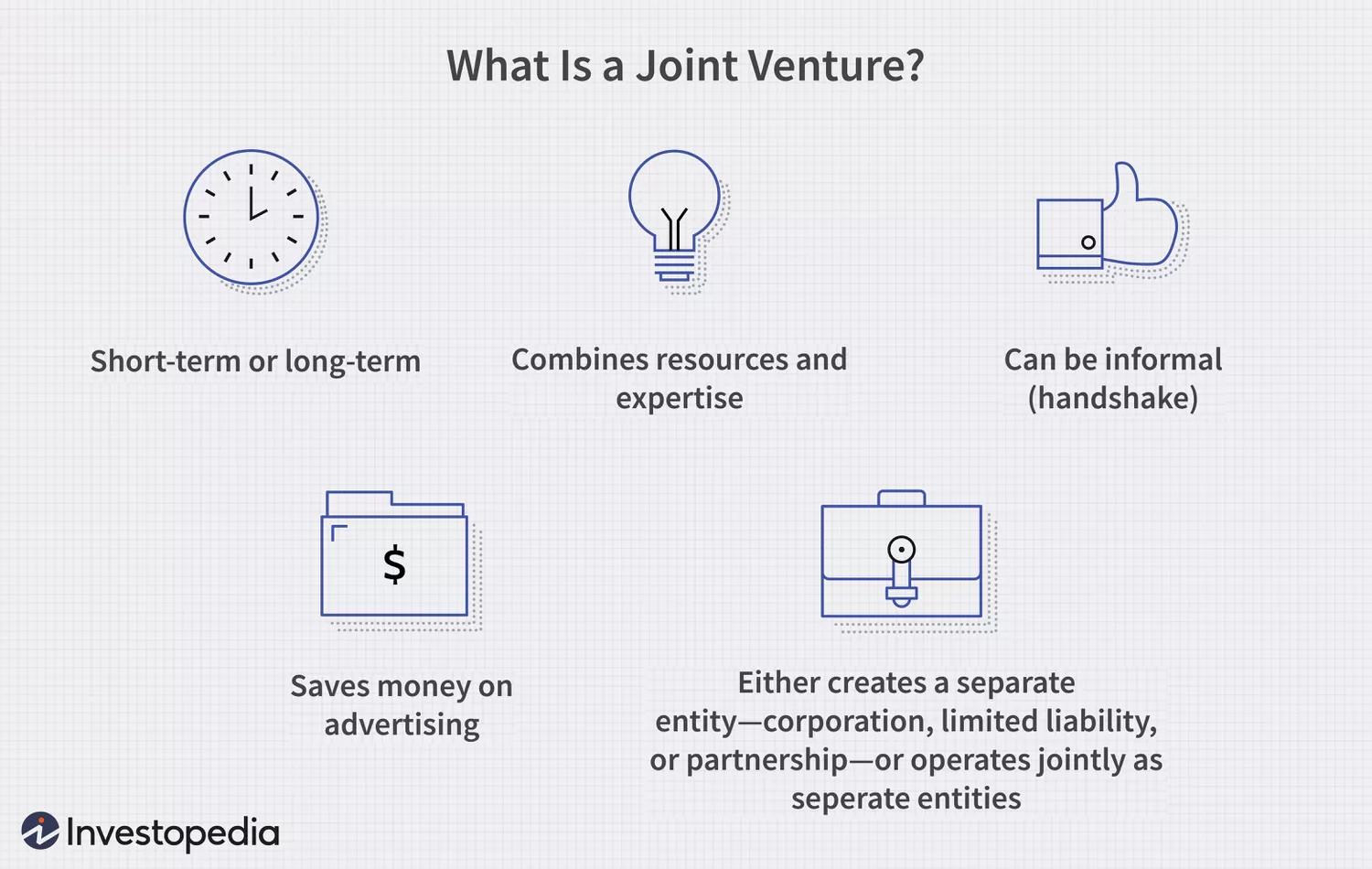

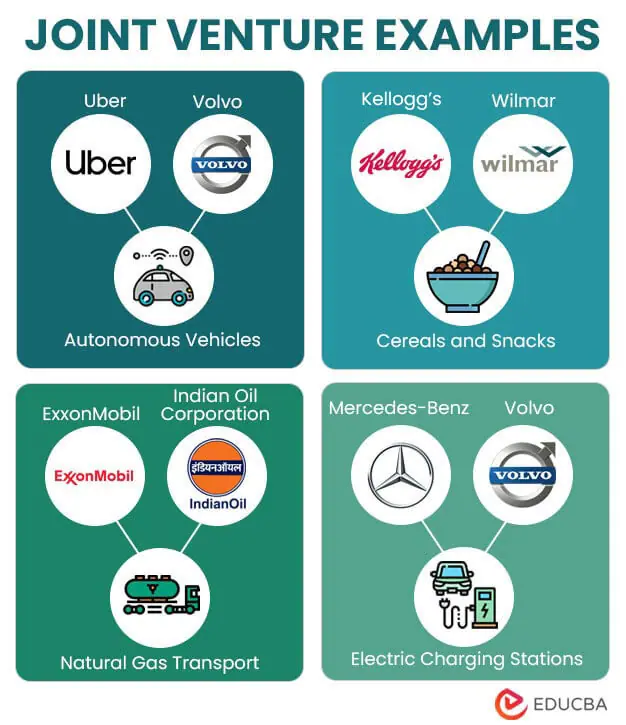

Joint Ventures

A joint venture is a strategic alliance where two or more parties undertake a business project together.

Image courtesy of investopedia

- Characteristics:

- Pooling of Resources: Partners contribute resources, expertise, and capital.

- Specific Purpose and Duration: Typically formed for a specific project or for a limited period.

- Shared Risks and Rewards: Profits, losses, and risks are shared according to the joint venture agreement.

- Separate Legal Structure: May form a separate legal entity distinct from the partners' existing businesses.

- Suitability: Best for companies looking to collaborate on specific projects or to enter new markets, combining strengths while limiting longer-term risks and commitments.

Image courtesy of educba

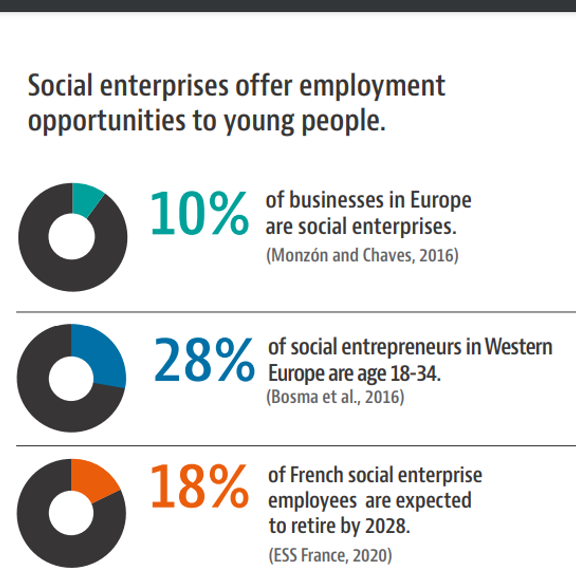

Social Enterprises

Social enterprises are businesses that operate with the primary goal of achieving social objectives.

- Characteristics:

- Social or Environmental Objectives: Committed to achieving specific social, environmental, or community objectives.

- Commercial Strategies: Uses business methods and practices to generate revenue.

- Reinvestment of Profits: Profits are primarily reinvested to support their social mission.

- Diverse Ownership Forms: Can be owned and operated by a wide range of entities, including non-profits, charities, or community groups.

- Suitability: Ideal for entrepreneurs and organizations focused on creating social value, often blending innovative business models with social goals.

Image courtesy of oecdcogito

Understanding Limited and Unlimited Liability

- Limited Liability: In companies, shareholders’ liability is limited to their investment. This protects personal assets but often involves more regulation.

- Unlimited Liability: In sole traders and partnerships, owners are personally responsible for all business debts, risking personal assets.

Implications of Transitioning Between Ownership Types

- Legal and Financial Impacts: Changing business structure can involve significant legal and financial changes, including new liability, tax implications, and ownership rights.

- Change in Control and Decision-making: Transitioning from a sole trader to a company can dilute personal control but provides limited liability.

- Risk Profile Alteration: Moving from unlimited to limited liability changes the risk profile of the business, affecting how it can raise capital and expand.

This detailed examination of business ownership types is vital for students to understand the implications of different structures in the business environment.

FAQ

Choosing between setting up as a sole trader or forming a partnership depends on several key factors. For individuals who prefer complete control and independence in their business operations, being a sole trader is more suitable. This structure is simpler, with fewer formalities and a straightforward decision-making process. However, sole traders bear all the risks and responsibilities alone, which can be a significant burden. In contrast, partnerships are ideal for those seeking to combine skills, knowledge, and resources with others. Partnerships allow for shared responsibility, risk, and expertise, potentially leading to a stronger business proposition. The decision also depends on the nature of the business and the industry. For example, professional services like law or accountancy often favour partnerships due to the collaborative nature of the work. Financial considerations also play a role; partnerships can provide more capital and shared financial responsibility, but they also involve shared liability. Ultimately, the choice hinges on the individual’s preference for independence versus collaboration, their risk tolerance, and the specific needs of the business.

Yes, a business can transition from a public limited company (PLC) to a private limited company (Ltd), but this process, known as 'privatisation,' involves significant legal, financial, and structural changes. The main implication of this transition is the change in the company's ownership and share distribution. In a PLC, shares are available to the general public and traded on a stock exchange. To become a private limited company, these shares must be bought back or consolidated, which can be a complex and costly process. Privatisation often results in a smaller, more concentrated group of shareholders and can provide the company with more privacy and control over its operations. However, it also means losing the potential capital and liquidity benefits of being listed on a stock exchange. The company may also face challenges in raising capital post-privatisation, as it will no longer have access to public equity markets. This transition requires careful planning, substantial financial resources, and legal expertise to navigate the complexities involved.

Tax implications vary significantly across different business ownership types. Sole traders and partnerships are subject to personal income tax on their business profits, as the business and owner are legally the same entity. This means that profits from the business are added to the individual's other income and taxed accordingly. In contrast, limited companies, both private (Ltd) and public (PLC), are taxed as separate legal entities. They pay corporation tax on their profits, and any dividends paid to shareholders are also subject to personal income tax. This can lead to double taxation – first on the company's profits and then on the dividends received by shareholders. However, limited companies may benefit from lower corporation tax rates and various tax-deductible expenses. Co-operatives are also taxed on profits, but they may have certain tax advantages if they meet specific criteria. Franchises, being individual businesses, are taxed based on the franchisee's business structure, whether it's a sole trader, partnership, or limited company.

In co-operatives, decision-making is democratic and typically follows the principle of 'one member, one vote,' regardless of the member’s financial contribution. This approach fosters equality among members and ensures that decisions reflect the collective interest of all members. Co-operatives often make decisions through member meetings or elected boards, focusing on community or member benefits rather than solely on profitability. In contrast, decision-making in joint ventures depends on the agreement between the parties involved. It usually reflects the proportion of investment or resources each party contributes. Joint ventures often establish a management committee or board comprising representatives from each partner, where decisions are made based on the venture's specific objectives. The focus is more on achieving the strategic goals of the joint venture, which may include profitability, market expansion, or specific project outcomes. Thus, while co-operatives emphasise democratic participation and community benefits, joint ventures focus on strategic objectives agreed upon by the investing partners.

Converting a sole trader business into a limited company offers several advantages, primarily revolving around limited liability and financial opportunities. As a limited company, the business becomes a separate legal entity, protecting the owner's personal assets from business liabilities. This structure enhances the business's credibility and can facilitate easier access to finance, as lenders may be more willing to offer funding to a limited company than to a sole trader. Additionally, a limited company might benefit from more favourable tax rates and the ability to reinvest profits into the business.

However, the transition also presents challenges. It involves more complex accounting, legal compliance, and administrative responsibilities. The owner must adhere to stricter reporting and disclosure requirements, including filing annual accounts and tax returns with Companies House and HM Revenue and Customs. The company’s financial information becomes public, reducing the privacy the owner enjoyed as a sole trader. Additionally, the process of setting up and maintaining a limited company can incur higher costs, including legal, accounting, and administrative expenses. Therefore, while transitioning to a limited company offers significant benefits in terms of liability and growth potential, it also requires a readiness to manage increased regulatory and financial complexities.

Practice Questions

A sole trader is a business owned by a single individual, offering complete control and simple setup but with unlimited liability, meaning personal assets are at risk for business debts. This structure is well-suited for small, low-risk businesses due to its simplicity and full decision-making autonomy. In contrast, a PLC is owned by shareholders with shares traded publicly, providing significant capital raising potential. The PLC's key feature is limited liability, protecting shareholders' personal assets. It's regulated more stringently, requiring transparent operations and governance. PLCs are ideal for larger businesses needing substantial capital and those aiming for high market visibility.

Operating as a franchise offers significant advantages, such as access to an established brand, proven business model, and ongoing support from the franchisor. This structure reduces the risk for new business owners and provides training and marketing assistance, which can be invaluable for those new to the industry. However, it also comes with drawbacks, such as limited operational autonomy since franchisees must adhere to strict operational guidelines set by the franchisor. Additionally, the initial investment can be substantial, and ongoing royalties reduce the net profits. Franchising suits individuals seeking the security of a known brand while willing to operate within predefined boundaries.